VALUATION FOR STARTUPS

Young and Start-Up Companies usually are small, they represent only a small part of the overall economy however they tend to have a disproportionately large impact on the economy for several reasons like Employment, Economic Growth, Innovation, Increased flow of foreign money, Decrease of Imports, Increase of Exports, etc.

Valuing companies early in the life cycle is difficult, partly because of the absence of operating history and partly because most young firms do not make it through these early stages to success. The valuation process hold importance for startups and entrepreneurs as it helps determine the fair amount of equity they have to give to an investor in exchange of funds . Also the process holds the same importance for investors as they need to know what percentage of shares they will receive in return for the amount they have invested.

The most fascinating interrogation comes forth is that with all such characteristics of startup companies; Is it really possible to value them?

Even though startups are notoriously hard to value accurately there are some approaches used to determine the company’s worth.

1.Cost-to-Duplicate Method-

This approach involves calculating how much it would cost to build another company just like it from scratch. It often looks at the physical assets to determine their fair market value. The cost-to-duplicate approach is often seen as a starting point for valuing startups since it is fairly objective. For a high-technology startup, it could be the costs to date of research and development, patent protection, and prototype development. This method requires extensive research, but it offers one of the most realistic valuation methods because it takes everything into consideration, from the initial idea to labor to relationship-building.

The big problem with this approach and company founders will certainly agree here is that it doesn’t reflect the company’s future potential for generating sales, profits, and return on investment. It doesn’t capture intangible assets, like brand value, that the venture might possess even at an early stage of development.

2.Market Multiple –

The Market Multiple Approach is one of the most popular startup valuation methods. The market multiple method works like most multiples do. Venture Capital investors like this approach, as it gives them a pretty good indication of what the market is willing to pay for a company. Basically, the market multiple approach values the company against recent acquisitions of similar companies in the market.

Let’s say mobile application software firms are selling for five times sales. Knowing what real investors are willing to pay for mobile software, you could use five-times multiple as the basis for valuing your mobile apps venture while adjusting the multiple up or down to factor for different characteristics. If your mobile software company, say, were at an earlier stage of development than other comparable businesses, it would probably fetch a lower multiple than five, given that investors are taking on more risk.

Unfortunately, there is a hitch: Comparable market transactions can be very hard to find. It’s not always easy to find companies that are close comparisons, especially in the startup market. Deal terms are often kept under wraps by early-stage, unlisted companies the ones that probably represent the closest comparisons.

3.Discounted Cash Flow (DCF) –

This valuation method applies to startups that are generating cash flows, and there is a certainty of cash flows in future. Discounted cash flow analysis then represents an important valuation approach. DCF involves forecasting how much cash flow the company will produce in the future and then, using an expected rate of investment return, calculating how much that cash flow is worth.

We begin with the fundamental notion that the discount rate used on a cash flow should reflect its riskiness, with higher-risk cash flows having higher discount rates. A higher discount rate is typically applied to startups, as there is a high risk that the company will inevitably fail to generate sustainable cash flows. Then the future free cash flows are estimated and discounted to the present value. And if the value obtained from this method is greater than the cost of investment, the investment opportunity is a positive one.

The problem with the DCF method is that it depends on an analyst’s ability to accurately predict future market conditions. The analyst then must make reasonable assumptions about long-term growth rates.

4.The Berkus Method (Valuation by Stage)-

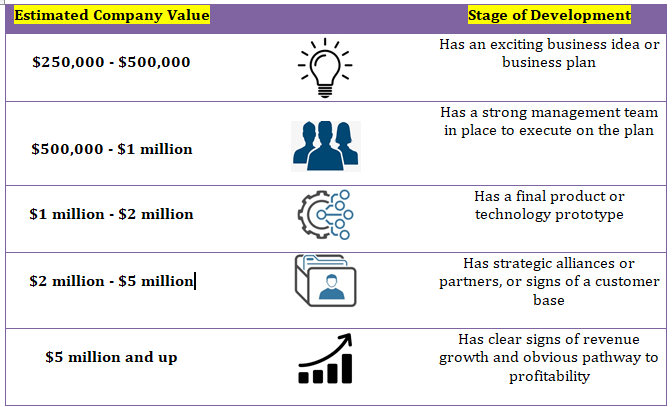

The Berkus Method was created by venture capitalist Dave Berkus to find valuations specifically for pre-revenue startups, i.e., businesses not yet selling their products at scale. The idea is to assign dollar amounts to five key success metrics found in early-stage startups. The Berkus Method works by assessing how your startup will perform in the five key criteria by assigning a number, a financial valuation, to each criterion. Finally, this is the development stage valuation approach, often used by angel investors and venture capital firms to quickly come up with a rough-and-ready range of company value.

Although it doesn’t take other market factors into account, the limited scope is useful for businesses looking for an uncomplicated tool. With the Berkus Method, the only financial projection you’ll need to make is the potential of your startup to generate over $20 million in revenues by your fifth year in business. Once a company is generating cash, this method is no longer applicable.

5.Scorecard Valuation Method-

The Scorecard Method is another option for pre-revenue businesses. It also works by comparing your startup to others that are already funded but with added criteria. First, you find the average pre-money valuation of comparable companies. Then, you’ll consider how your business stacks up according to the following qualities.

- Strength of the team: 0-30%

- Size of the opportunity: 0-25%

- Product or service: 0-15%

- Competitive environment: 0-10%

- Marketing, sales channels, and partnerships: 0-10%

- Need for additional investment: 0-5%

- Other: 0-5%

A venture capitalist firm would assign weights to each of these factors and compare them to competitors. You’d get the factors for each category by multiplying the weight for each category by the startup’s relative position. You’ll then assign each quality a comparison percentage. Essentially, you can be on par (100%), below average (<100%), or above average (>100%) for each quality compared to your competitors.

For example, you give your ecommerce team a 150% score because it’s complete, fully trained, and has experienced developers and marketers, some from rival businesses. You’d multiply 30% by 150% to get a factor of .45.

Do this for each startup quality and find the sum of all factors. Finally, multiply that sum by the average valuation in your business sector to get your pre-revenue valuation.

6.Risk Factor Summation Method-

The Risk Factor Summation method is used mostly for pre-revenue, pre-money startups. This method values a startup by taking into quantitative consideration all risks associated with the business that can affect the return on investment. Return on Investment (ROI) is a performance measure used to evaluate the returns of an investment or compare efficiency of different investments.

Unlike the Berkus method, where startup company valuation is done using only five key criteria, the Risk Factor Summation Method (RFS method) considers a wide range of criteria to reach the pre-money valuation. You start with an average valuation for your company based on similar companies in your area and region. Then, you compare the different risk factors for you own startup on a range from very low to very high.Lower risks increase the valuation for your company while higher risks decrease the valuation.

To improve your valuation, you can try to work on your risks and develop plans how to cover or reduce them. After taking into consideration all kinds of risk and implementing the “risk factor summation” to the initial estimated value of the startup, the final value of the startup is determined.

Different risks that this method considers are:

- Stage of the business

- Investment and Capital Accumulation Risk

- Manufacturing risk

- Sales and marketing risk

- Management

- Reputation risk

- Technology risk

- Competition risk

- International risk

- Legislation/Political risk

- Litigation risk

- Legal Environmental Risk

- Funding/capital raising risk

- A potentially profitable exit

7.Venture Capital Method-

First outlined by Professor Bill Sahlman in 1987 at Harvard Business School, the Venture Capital Method is implemented from the viewpoint of the investors.

In this method, valuation is done based on two things:

- Expected ROI

- Expected Sale Value after X years

There are two formulas you’ll use to work toward your valuation:

- Anticipated Return on Investment (ROI) = Terminal Value ÷ Post-Money Valuation

- Post-Money Valuation = Terminal Value ÷ Anticipated ROI

First, you’ll calculate your startup’s terminal value, or the expected selling price after the VC firm has invested. You can find this using estimated revenue multiples for your industry or the price-to-earnings ratio. Determine the anticipated ROI, such as 10x, and plug everything in to find your post-money valuation. This method is useful if you have an investor who is specifying a desired ROI as a condition of selling the company.

Conclusion

Startup valuation can be complicated, but these methods we’ve listed here are among the most common and can help get you started. We the professionals having expertise in this dimension can help you to estimate the value of your own startup or acquire a startup as a growth strategy or invest in a startup.