What is the Concept of Tax Deducted at Source (TDS)?

Tax Deducted at Source (TDS) is a system implemented by the Income Tax Department where income tax is deducted at the time of making specified payments such as rent, commission, professional fees, salary, interest, etc. The person making these payments deducts the tax and sends it directly to the Central Government. This way, the government collects tax right when income is earned, making the process smoother and more efficient.

Example: ABC Pvt Ltd makes a payment for office rent of Rs 50,000 per month to XYZ (owner of the property). TDS is required to be deducted at 10%. ABC Pvt ltd must deduct TDS of Rs 5,000 and pay the balance of Rs 45,000 to XYZ.

Who is Liable to Deduct TDS?

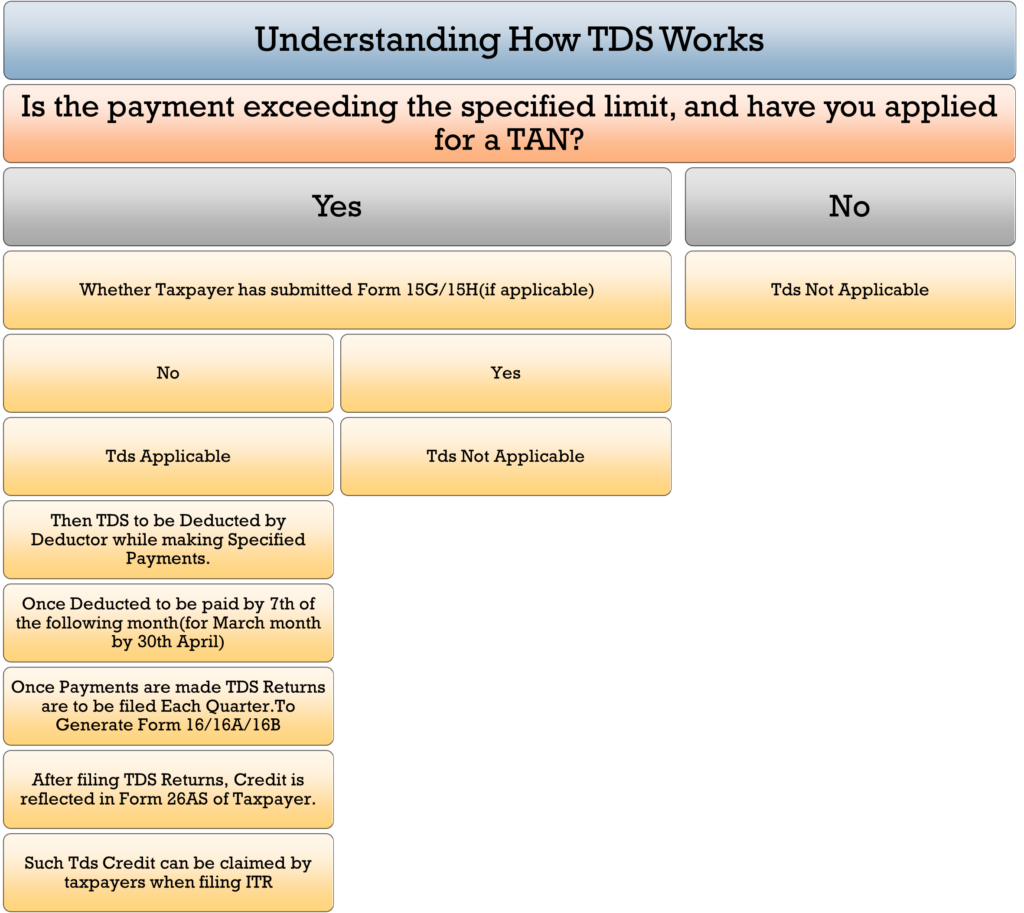

According to the Income Tax Act, any company or individual is required to deduct tax at source (TDS) if the payment exceeds a specified limit. However, to be authorized to deduct TDS, the person or entity must first obtain a Tax Deduction Account Number (TAN). TAN stands for Tax Deduction Account Number. It is a unique 10-digit alphanumeric identifier that must be obtained by all persons or entities responsible for deducting or collecting tax.

When should TDS be deducted and paid?

The concept of TDS is based on a simple principle: tax should be deducted at the time the payment becomes due or when the actual payment is made, whichever occurs earlier. Tax Deducted at Source (TDS) must be deposited with the government by the 7th of the following month. For example, TDS deducted in May is due by the 7th of June. However, TDS deducted in March can be deposited by the 30th of April. For property purchases, the TDS payment is due 30 days from the end of the month in which it is deducted.

What is TDS Return?

TDS return can be best described as the quarterly statement or summary of all TDS-related transactions made during the specific quarter. Typically, it comprises details of the TDS collected and deposited to the Income Tax Authority by the deductor. The essential details disclosed in a TDS return statement include the following –

- Deductor and deductee’s PAN.

- Particulars of TDS paid

- Challan details

Types and Due Dates of TDS returns

| Form No | Transactions reported in the return | Due date |

| Form 24Q | TDS on Salary | Q1 – 31st July Q2 – 31st October Q3 – 31st January Q4 – 31st May |

| Form 26Q | TDS on all payments except salaries | Q1 – 31st July Q2 – 31st October Q3 – 31st January Q4 – 31st May |

| Form 27Q | TDS on all payments made to non-residents except salaries | Q1 – 31st July Q2 – 31st October Q3 – 31st January Q4 – 31st May |

| Form 26QB | TDS on sale of property | 30 days from the end of the month in which TDS is deducted |

What is a TDS certificate?

A TDS certificate is a document issued to the taxpayer by the deductor (the person responsible for deducting tax at source) after filing the TDS return. It serves as proof of tax deducted at source on the taxpayer’s income. Forms such as Form 16, Form 16A, and Form 16B are examples of TDS certificates. The deductor is required to provide the TDS certificate to the assessee from whose income TDS was deducted during the payment process.

- Form 16- TDS on salary payment

- Form 16A- TDS on non-salary payments

- Form 16B- TDS on sale of property

What is 26AS?

When TDS (Tax Deducted at Source) returns are filed by the deductor, the amount of TDS deducted is reflected in the taxpayer’s Income Tax login and can be viewed in Form 26AS. In essence, once TDS returns are filed, the TDS amount is credited to the respective person’s PAN (Permanent Account Number). This credit is visible in Form 26AS, and the taxpayer can claim it when filing their Income Tax returns.

Can I request tax deductors to not deduct TDS from my payment?

Non-deduction of TDS is possible if your income is below the minimum taxable limit. If your income is below Rs. 2.5 lakh (or the applicable limit for your category), you can submit Form 15G (for individuals) or Form 15H (for senior citizens) to the deductor, declaring your income. Additionally, you can apply to the Assessing Officer using Form 13 to obtain a certificate for lower or nil deduction of taxes. However, if your income exceeds the minimum taxable limit, you cannot request an exemption from TDS.

How to determine the correct section and rate for deducting TDS?

To determine the appropriate section for deducting TDS and the corresponding rate, you can refer to the detailed guidelines provided by the Income Tax Department. The attached link contains comprehensive information on various TDS sections and their applicable rates.

Penalty provisions for non-deduction of TDS.

- If a person responsible for deducting TDS fails to do so, up to 30% or the entire expenditure can be disallowed when calculating taxable profits.

- TDS must be deducted at the time of payment or when it is due; late deductions incur interest at 1% per month of the TDS amount.

- TDS must be paid to the government by the 7th of the following month after deduction; late payments incur interest at 1.5% per month of the TDS amount.

- TDS returns must be filed by the end of the month following each quarter, with a fee of Rs 200 per day for late filing, up to the amount of the TDS.

- The Assessing Officer can impose a penalty of Rs 10,000 to Rs 1,00,000 for failing to file TDS returns on time, in addition to penalties under section 234E.

Note: We have also enclosed one flow chart below for reference and better understanding.